Revenue recognition rules explained: Principles, steps, and examples

Revenue recognition rules determine when your financials reflect real value delivered, not just cash collected. This guide breaks down ASC 606 and IFRS 15 for B2B finance teams managing subscriptions, usage-based pricing, and complex contracts. We'll cover the five-step model, common pitfalls, and how automation turns compliance from a burden into a foundation for trustworthy reporting.

What are revenue recognition rules?

Revenue recognition rules are the accounting standards that tell you exactly when to record revenue on your financial statements. They exist to ensure your books reflect actual value delivered to customers—not just cash collected. For B2B companies with subscriptions, usage-based pricing, or multi-year contracts, these rules determine how revenue flows through your profit and loss (P&L) statement over time.

The core concept is simple: you can't book revenue just because a customer paid you. You book it because you earned it. This is the difference between accrual accounting (revenue recorded when earned) and cash accounting (revenue recorded when received). Most B2B companies that are audited, investor-backed, or lender-backed operate on accrual accounting, which means a $120,000 annual contract paid upfront gets recognized as $10,000 per month—not all at once.

This separation of billing from revenue creates real operational complexity. Your invoice says one thing. Your revenue schedule says another. And your finance team is responsible for keeping both accurate and reconciled. Modern revenue automation platforms like Tabs address this by connecting contract terms directly to Revenue Recognition logic—so contract language is parsed, key terms are classified, and recognition schedules reflect not just what was billed, but what was earned and when.

Why revenue recognition rules matter for B2B finance

Get revenue recognition wrong, and everything downstream breaks. Your forecasts become unreliable. Your board loses confidence. Your auditors start asking uncomfortable questions.

Why it matters: Revenue Recognition is the foundation for auditability, forecasting credibility, and investor trust—especially when billing and delivery don't line up.

For B2B companies with complex contracts—hybrid billing models, variable usage, milestone payments—the stakes compound. Recognize revenue too early, and you inflate current performance while borrowing from future periods. Recognize it too late, and you understate growth during critical fundraising windows.

The consequences show up in predictable ways:

- Restatement risk: Errors discovered post-close require restating historical financials, signaling weak controls to investors

- Audit friction: Missing documentation or inconsistent policies slow external reviews and distract your team

- Forecasting gaps: Inaccurate historical data undermines forward-looking plans for cash runway and hiring

- Investor scrutiny: Inconsistent reporting erodes trust, potentially impacting valuation during fundraising

The fix isn't more spreadsheets or more headcount. It's ensuring that recognition logic is tied directly to contract terms and applied consistently across every deal. That's where automation becomes essential—not as a nice-to-have, but as the foundation for trustworthy financials.

GAAP and IFRS revenue recognition standards

Two frameworks govern revenue recognition globally: ASC 606 (US Generally Accepted Accounting Principles, or GAAP) and IFRS 15 (International Financial Reporting Standards, or IFRS). Both were developed jointly to create consistency across borders and industries. They share the same five-step model, but differ in how prescriptive the guidance is.

ASC 606 applies to all US public and private companies. It tends to be more detailed, with specific rules for edge cases. IFRS 15 governs international entities and is more principles-based, leaving more room for judgment. According to KPMG's revenue handbook, the IASB concluded the standard is working as intended, though some areas remain challenging in practice.

| Aspect | ASC 606 (US GAAP) | IFRS 15 (International) |

|---|---|---|

| Governing body | Financial Accounting Standards Board (FASB) | International Accounting Standards Board (IASB) |

| Effective date | Public: 2018 / Private: 2019 | 2018 |

| Scope | US entities | International entities |

| Core model | Five-step framework | Five-step framework |

| Key difference | More prescriptive | More principles-based |

If you operate internationally or have global investors, you may need to satisfy both standards. The good news: because they share the same core model, getting one right usually means you're close on the other.

The revenue recognition principle under GAAP

The fundamental principle is straightforward: recognize revenue when control of goods or services transfers to the customer, in an amount reflecting the consideration you expect to receive.

Control means the customer can direct the use of and obtain benefits from what you delivered. This is different from the old standard, which focused on "risks and rewards." Now, the question is simpler: can the customer use it?

For a SaaS company, signing a contract isn't a revenue event. Sending an invoice isn't either. The revenue event happens when the customer can actually access and use your software. If you sell a 12-month subscription, the customer consumes that benefit continuously—so you recognize revenue monthly, regardless of when they paid.

One more requirement: collectability must be probable. You can't recognize revenue if there's significant doubt you'll actually collect payment.

ASC 606 five-step revenue recognition model

ASC 606 establishes a five-step framework that applies to every contract with a customer. Each step requires significant judgment, especially for B2B companies with bundled offerings or variable pricing.

1. Identify the contract with the customer

A contract exists when there's a binding agreement with commercial substance, clear payment terms, and probable collectability. Watch for termination clauses. If a customer can cancel without penalty, the contract duration for accounting purposes may be shorter than the stated term.

2. Identify performance obligations

List every distinct promise to deliver goods or services. If a contract includes software, implementation, and support—areas KPMG identifies as requiring significant judgment—determine whether each is a separate obligation or part of a single bundle. The test: can the customer benefit from the item on its own?

3. Determine the transaction price

Calculate the total consideration you expect to receive. This includes fixed amounts plus variable elements like discounts, rebates, or usage-based fees. For contracts with variable components, you must estimate the most likely amount and update that estimate each period.

4. Allocate the transaction price

Distribute the total price across each performance obligation based on standalone selling prices. If you sell a bundle at a discount, that discount gets allocated proportionally—not applied entirely to one item.

5. Recognize revenue when obligations are satisfied

Record revenue as each obligation is fulfilled. This happens either at a point in time (delivering hardware) or over time (providing ongoing access to software).

Revenue recognition timing over time vs. point in time

How you recognize revenue depends on when the customer receives value. This distinction drives the mechanics of your revenue schedules.

- Over time: The customer receives and consumes benefits as you perform. This applies to SaaS subscriptions, maintenance contracts, and ongoing services.

- Point in time: Control transfers at a specific moment. This applies to hardware sales, perpetual licenses, or one-time deliverables.

To qualify for over time recognition, your contract must meet at least one of these criteria:

- The customer simultaneously receives and consumes benefits as you perform

- Your performance creates or enhances an asset the customer controls

- Your performance doesn't create an asset with alternative use, and you have an enforceable right to payment for work completed

If none apply, you default to point-in-time recognition.

Compliance requirements for public and private companies

The core principles apply to everyone, but the compliance burden differs. Public companies face Securities and Exchange Commission (SEC) reporting requirements, Sarbanes-Oxley (SOX) controls, and quarterly deadlines. Private companies have more flexibility—but still need audit-ready books if they have investors or lenders.

| Requirement | Public companies | Private companies |

|---|---|---|

| ASC 606 adoption | Mandatory since 2018 | Mandatory since 2019 |

| SEC filings | Required quarterly and annually | Not applicable |

| SOX compliance | Required | Typically not required |

| External audit | Required | Often required by investors |

| Disclosure depth | Extensive footnotes | Less prescriptive |

Both must maintain documentation sufficient to support their recognition positions. You need to prove not just the final numbers, but the judgments made to arrive at them.

Revenue recognition examples for subscriptions and bundles

Applying the five-step model to real scenarios clarifies how these rules work in practice.

Annual SaaS subscription

A customer signs a one-year seat-based subscription for $60,000, billed upfront. The performance obligation is providing access to the platform. Since the customer consumes this benefit continuously, you recognize $5,000 monthly. The remaining balance sits as deferred revenue until earned.

Bundled software and implementation

A customer purchases a $50,000 subscription plus $10,000 implementation. If the software works without the implementation, these are distinct obligations. You allocate the $60,000 based on standalone selling prices, recognize implementation revenue when complete, and recognize software revenue ratably over the term.

Usage-based contract with minimum commitment

A customer commits to $120,000 annually with overage billing for excess usage. The minimum is recognized ratably ($10,000/month) as a standing-ready obligation. Overages are recognized in the period usage occurs.

Common revenue recognition challenges and how to handle them

B2B finance teams encounter scenarios that don't fit neatly into simple models. These edge cases are where manual processes break down.

- Variable consideration: Contracts with bonuses, discounts, or penalties require estimating the transaction price and updating it each period

- Contract modifications: Mid-term upgrades or extensions require determining whether to treat changes as a new contract or a modification of the existing one

- Bundled offerings: Allocating prices across items that are never sold separately requires defensible methodologies

- Data fragmentation: Contract terms live in PDFs, usage data sits in engineering logs, and invoices are in the ERP—with no single source of truth

- Multi-entity complexity: International subsidiaries require reconciling currencies, tax treatments, and intercompany transactions

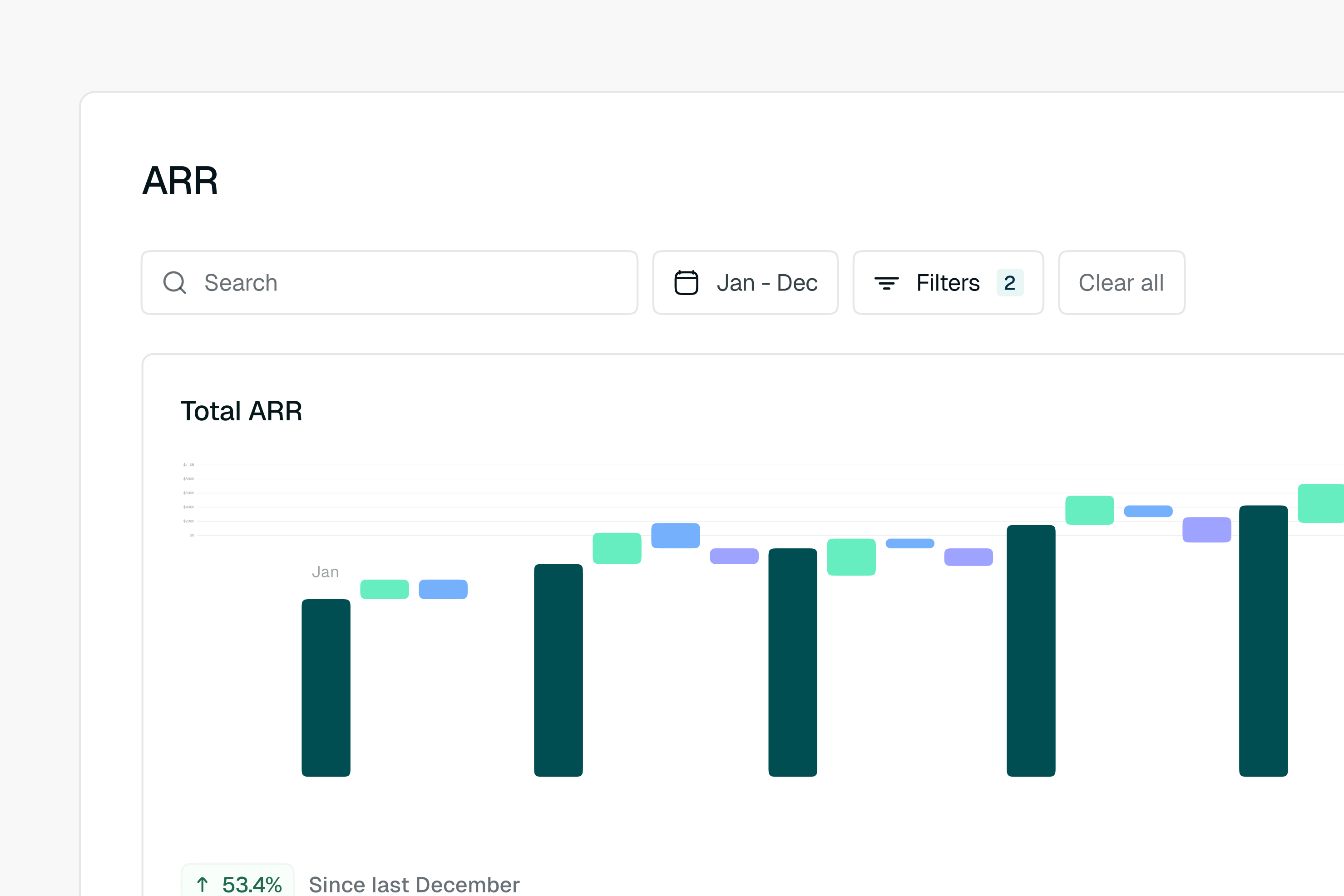

By using AI billing agents to ingest contract terms and unify them with billing and usage data, Tabs creates what it calls the Commercial Graph. This is a unified record that links deal entities (customer, products, dates, pricing, and obligations) and maps them to billing and Revenue Recognition workflows. This means complex modifications or variable terms can be automated with configurable review and approval workflows—so you preserve commercial nuance, consistency, and auditability in Revenue Recognition.

Revenue recognition automation for ASC 606 compliance

As transaction volumes grow and billing models evolve, manual revenue recognition becomes a bottleneck. Automation replaces the patchwork of spreadsheets and manual journal entries with a systematic, audit-ready process with audit-grade transparency.

What automation enables:

- Contract ingestion: AI extracts billing terms, performance obligations, and pricing directly from signed contracts

- Recognition scheduling: Rules automatically determine timing and amounts based on contract structure

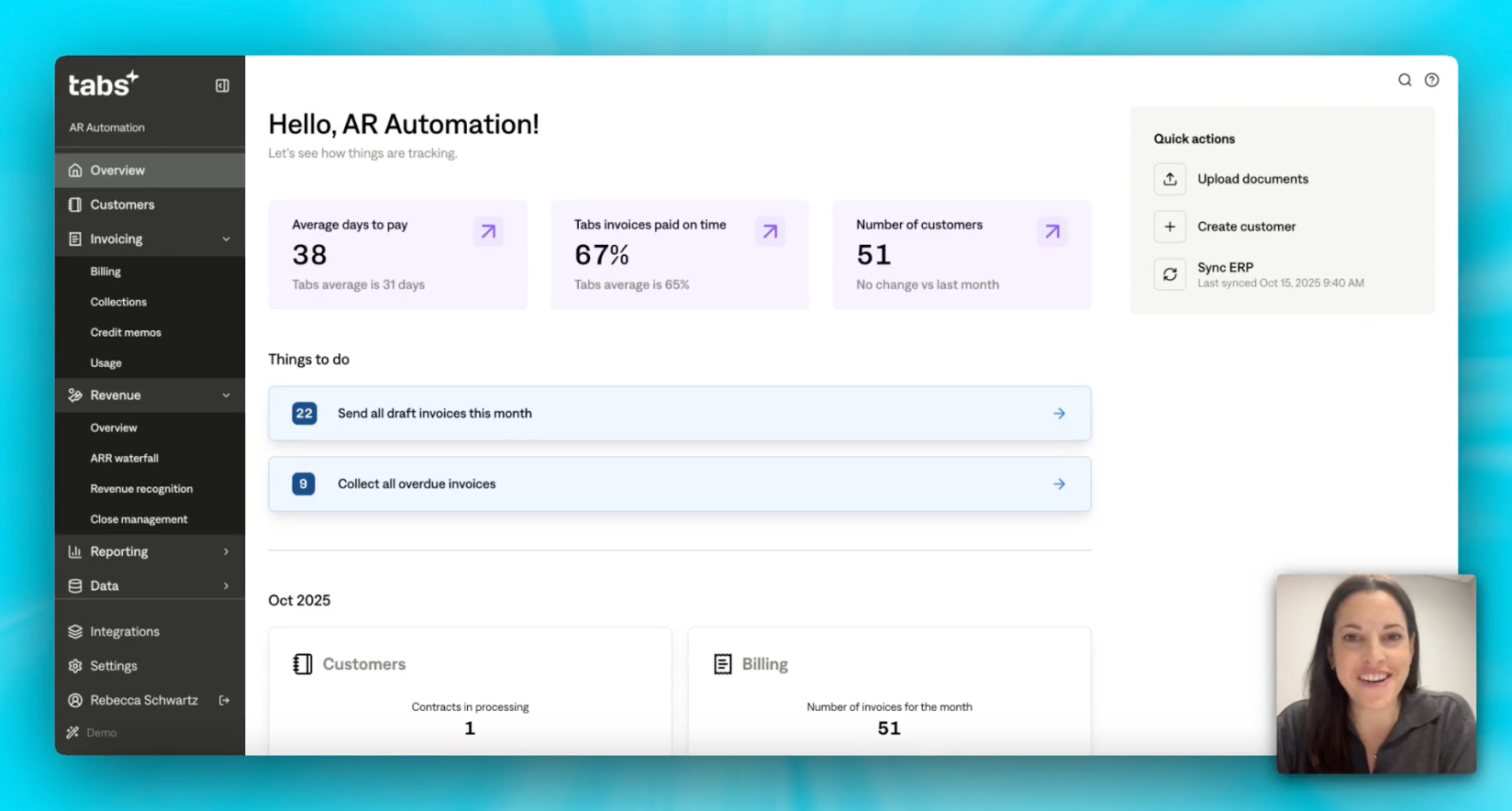

- ERP synchronization: Journal entries flow to NetSuite, QuickBooks, or Sage Intacct without manual intervention

- Audit trail: Every decision is logged with supporting documentation

Tabs differentiates by providing commercial context—not just extracting fields, but classifying contract language and mapping it to the correct billing and Revenue Recognition treatment. A "platform fee" behaves differently than a "setup fee." Tabs translates those nuances into compliant workflows with minimal custom code, supporting controlled exceptions when your policies require a manual review or override.

Revenue recognition audit readiness and controls

Audit readiness is a continuous discipline, not a year-end scramble. Auditors focus on revenue because it's the most critical number on your financials. They want evidence that your policies are compliant and applied consistently.

Essential controls:

- Cutoff procedures: Prove revenue was recorded in the correct period by testing transactions near period boundaries

- Reconciliation cadence: Monthly reconciliation between subledger and general ledger, with variances investigated immediately

- Documentation standards: Maintain clear links between contracts, invoices, and revenue schedules

- Policy consistency: Apply the same methods across similar contract types

- Access controls: Restrict who can modify recognition rules or override calculations

Frequently asked questions

What is the difference between billing a customer and recognizing revenue?

Billing is sending an invoice requesting payment. Revenue recognition is recording that value as earned on your financial statements. You might bill $12,000 in January for an annual subscription but only recognize $1,000 that month—the rest is deferred until earned.

How do SaaS companies recognize subscription revenue under ASC 606?

SaaS companies typically recognize subscription revenue ratably over the contract term because customers receive benefits continuously. Other elements like implementation or usage overages have different timing—services are recognized as performed, overages when usage occurs.

What are the consequences of recognizing revenue incorrectly?

Errors can force restatements of historical financials, delay audits, and erode investor confidence. For public companies, incorrect recognition can trigger SEC scrutiny. Beyond compliance, it damages the credibility of your entire finance function.

Explore how Tabs can help you operationalize signed contracts and automate Revenue Recognition with audit-grade transparency.