How to calculate annual recurring revenue (ARR) the right way

For finance leaders at B2B companies, ARR is the metric that drives valuations, board conversations, and strategic planning. This guide breaks down exactly how to calculate ARR, when to use each formula, and how to avoid the common mistakes that lead to inflated numbers and unreliable forecasts.

What is annual recurring revenue (ARR)?

Annual recurring revenue (ARR) is the total value of your recurring subscription contracts, normalized to a one-year period. That means that if a customer signs a three-year deal worth $36,000, your ARR from that contract is $12,000. That $12k is the amount you can expect to generate each year from the recurring subscription.

ARR strips away the noise of one-time fees and variable charges to reveal the predictable core of your business. It answers a simple question: if nothing changes, how much recurring revenue will you generate over the next 12 months?

For B2B companies, ARR is the metric that matters most. Investors use it to value your company. Boards use it to measure growth. Finance teams use it to forecast cash flow and plan headcount. Get it wrong, and every downstream decision—from hiring to fundraising—starts on shaky ground.

But here's where most teams stumble: they include revenue that doesn't belong.

- Included in ARR: Subscription fees, recurring platform charges, annual maintenance contracts, and recurring add-ons.

- Excluded from ARR: One-time implementation fees, professional services, hardware sales, and setup charges.

The distinction matters because ARR is supposed to represent revenue you can count on repeating. One-time fees inflate the number and create a false sense of stability.

Modern Revenue Automation platforms like Tabs solve this problem by operationalizing signed contracts as the source of truth for recurring versus non-recurring revenue. Tabs uses AI models trained on your contracts, CRM, and payment platforms to extract key terms from signed agreements. Line items are classified based on commercial context—billing cadence, renewal language, ramp clauses, and bundled components—so recurring and non-recurring revenue are categorized consistently for ARR.

How to calculate ARR

There are two primary methods for calculating ARR. The right choice depends on how complex your pricing model is and how much visibility you need into the drivers of revenue change.

Use the net ARR formula

The most accurate approach tracks the movement of revenue across four categories. Finance teams call this the "roll-forward" method because it shows how ARR evolves from the beginning to the end of a period.

The formula:

Beginning ARR + New ARR + Expansion ARR − Churned ARR = Ending ARR

Each component tells you something specific about your business:

- Beginning ARR: The total annual value of active subscription contracts at the start of the period.

- New ARR: Revenue from customers who signed their first contract during the period.

- Expansion ARR: Additional revenue from existing customers—upsells, cross-sells, price increases, or added seats.

- Churned ARR: Revenue lost when customers cancel or downgrade their subscriptions.

This method forces you to understand why your revenue is changing. A company growing ARR by $1 million could be adding $2 million in new business while losing $1 million to churn. That's a very different story than adding $1 million with zero churn.

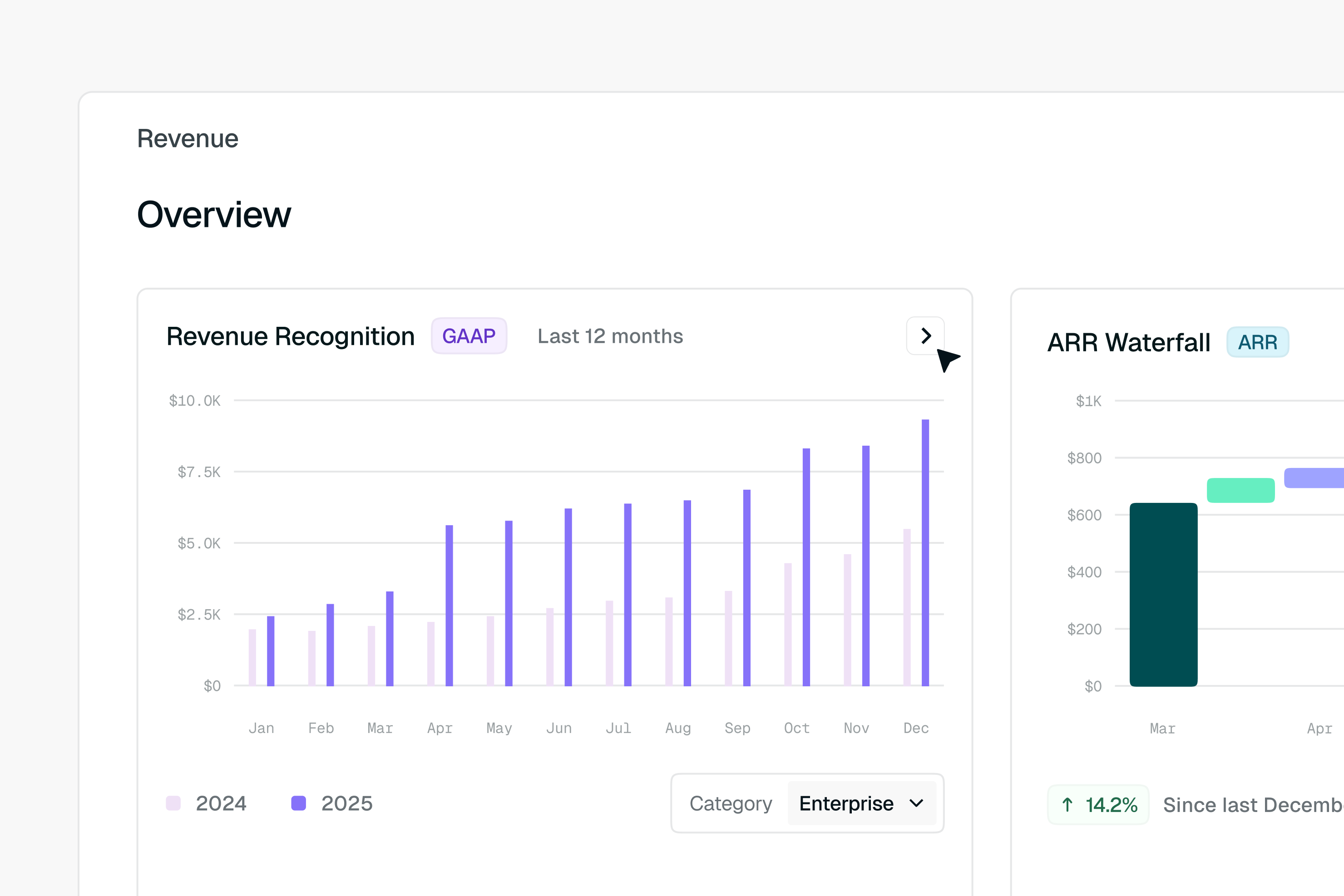

The challenge is that tracking these components requires clean, connected data. You need to know exactly when a contract started, when it expanded, and when it churned—down to the line item. Tabs builds what it calls a "Commercial Graph" for each customer, linking signed contract terms with connected usage feeds and payment history. This enables you to calculate ARR consistently at the line-item level.

Why it matters: The net ARR formula reveals the quality of your growth, not just the quantity.

Multiply MRR by 12

The second method is a shortcut. You take your Monthly Recurring Revenue (MRR)—the sum of all monthly subscription fees—and multiply by 12.

The formula:

MRR × 12 = ARR

This works well for early-stage companies with simple, consistent monthly pricing. If every customer pays the same amount every month and nothing changes, the math holds.

But the shortcut breaks down quickly. If you have an unusually strong month, multiplying a single month's MRR by 12 can overstate your annualized run rate. If you have usage-based pricing, a spike in consumption creates an artificially high ARR that you won't sustain.

- When it works: Stable monthly subscriptions with minimal churn or expansion.

- When it fails: Seasonal businesses, usage-based models, or companies with significant mid-contract changes.

For companies with hybrid or usage-based billing, this method is risky. It treats a temporary spike as permanent recurring revenue. Finance teams often try to fix this by manually normalizing the data in spreadsheets—calculating trailing averages, adjusting for anomalies. That manual work introduces errors and takes time.

Why it matters: MRR × 12 is fast but fragile. Use it only when your revenue is genuinely stable.

Turn contracts into precise ARR

ARR calculation examples

Formulas make more sense when you see them in action. Below are two scenarios that show how different pricing models affect the calculation.

Annual subscription example

A B2B software company sells a platform license. They have 100 customers, each on a one-year contract worth $12,000.

Calculation:

100 customers × $12,000 in annual contract value per customer = $1,200,000 ARR

The billing frequency doesn't change the ARR. Even if these customers pay $1,000 per month, the ARR is still $1.2 million because the contract commits them to a full year.

This is the simplest scenario. The math is clean because the pricing is fixed and the terms are uniform.

Why it matters: When contracts are straightforward, ARR calculation is straightforward.

ARR bridge example (new, expansion, and churn)

The net ARR formula is easiest to trust once you see it move real numbers. Consider a company that starts the year with $1,000,000 in ARR, signs new customers, expands existing accounts, and loses some revenue to churn.

Calculation:

$1,000,000 (beginning ARR) + $250,000 (new ARR) + $120,000 (expansion ARR) − $90,000 (churned ARR) = $1,280,000 (ending ARR)

The bridge shows the quality of that growth, not just the headline number. Net ARR grew by $280,000, but the underlying story is $370,000 of new and expansion revenue offset by $90,000 of churn—a distinction the MRR × 12 shortcut hides entirely.

Why it matters: An accurate bridge depends on knowing exactly when each contract started, expanded, or churned at the line-item level, which is the same commercial context Tabs applies when it turns signed contracts into precise ARR.

Usage plus subscription example

Now consider a company with hybrid pricing. They charge a $10,000 annual platform fee plus a variable fee based on API usage. This is where manual calculations get messy.

You need to separate the fixed revenue from the variable revenue:

- Fixed component: 50 customers × $10,000 platform fee = $500,000.

- Usage component: Calculate a trailing three-month average of usage revenue, then annualize it.

If the average monthly usage revenue over the last three months is $20,000:

$20,000 × 12 = $240,000 usage ARR

Total ARR:

$500,000 (fixed) + $240,000 (usage) = $740,000

The usage component requires judgment. Do you use a three-month average? Six months? Do you exclude outliers? These decisions affect your ARR, and different people on your team might make different choices.

Tabs handles this complexity natively. For hybrid contracts, Tabs maps fixed fees and usage terms from the signed agreement to billing treatment (for example, base platform fees billed annually while usage is annualized from a defined trailing average) and calculates ARR using connected consumption data. All without forcing your team into one-off spreadsheet logic.

Why it matters: Hybrid pricing is increasingly common, but most other finance stacks weren't built for it. Tabs is.

ARR vs MRR and revenue

ARR, MRR, and GAAP revenue are related but serve different purposes. Confusing them leads to reporting errors and awkward conversations with your board.

ARR is a forward-looking operational metric. It tells you what you expect to earn over the next year based on current contracts.

MRR is the monthly version of ARR. It's useful for tracking short-term trends and month-over-month growth.

GAAP revenue is an accounting measure reported under Generally Accepted Accounting Principles (GAAP). It measures what you've actually earned based on service delivery, following rules like ASC 606. GAAP revenue is backward-looking and can include portions of upfront fees that are allocated under ASC 606—which requires significant judgment and estimation—and recognized over time.

| Metric | Direction | Purpose | Includes one-time fees? |

|---|---|---|---|

| ARR | Forward-looking | Forecasting, valuation | No |

| MRR | Current snapshot | Monthly trends | No |

| GAAP revenue | Backward-looking | Financial statements, audits | Yes (allocated and recognized over time, when applicable) |

How ARR compares to MRR

MRR is the building block of ARR. You calculate MRR by summing the monthly fees from all active subscriptions. ARR is simply MRR annualized.

But they're used for different conversations. MRR helps you manage monthly sales targets and track immediate churn impacts. ARR is what you present to investors and use for annual planning.

The relationship seems simple—MRR × 12 = ARR—but it only holds when your revenue is stable. For companies with fluctuating usage or seasonal patterns, you need to calculate ARR using the net formula rather than relying on a single month's MRR.

Why it matters: Use MRR for operations. Use ARR for strategy.

Why ARR matters for finance leaders

ARR isn't just a number on a dashboard. It's the foundation for nearly every strategic decision a finance leader makes.

Forecasting: Accurate ARR lets you project cash flow and runway. If your ARR is inflated by bad data, you might overspend and run out of cash before your next fundraise.

Valuation: Investors value subscription businesses as a multiple of ARR. McKinsey's analysis of B2B tech companies found top-quartile performers achieve 24x enterprise-value-to-revenue multiples versus 5x for bottom-quartile peers. A clean, verifiable ARR number directly impacts how much capital you can raise and at what terms.

Board reporting: Boards expect to see the ARR bridge—the breakdown of beginning ARR, new, expansion, and churn. They want to understand the quality of your growth, not just the headline number.

Retention analysis: ARR enables you to calculate Net Revenue Retention (NRR), which shows whether your existing customer base is growing or shrinking over time.

The problem is that ARR is only as reliable as the data behind it. If your finance team is manually pulling contract terms from PDFs, entering them into spreadsheets, and reconciling against billing records, errors creep in. Revenue leakage hides in these handoffs—missed renewals, incorrect price uplifts, forgotten start dates.

This is where Tabs provides a distinct advantage. Tabs doesn't just calculate ARR. It becomes a system of intelligence for your contract-to-cash data, building a complete commercial record for each customer. By using AI to ingest contracts, Tabs interprets terms like payment schedules, renewals, ramps, and uplift clauses and translates them into the billing and Revenue Recognition actions your finance team needs. With Tabs, signed agreements turn into billing schedules and ASC 606 Revenue Recognition workflows automatically, using the commercial terms in the contract to drive downstream operations.

Your ARR becomes a precise calculation based on actual commercial agreements, not an approximation derived from manual data entry. Finance teams can stop chasing down data and start using ARR to drive business strategy.

Frequently asked questions

Is ARR always calculated by multiplying MRR by 12?

No. Multiplying MRR by 12 is a shortcut that works for companies with stable, consistent monthly revenue. If your business has seasonal fluctuations, usage-based pricing, or significant mid-contract changes, you should use the net ARR formula instead. That approach tracks new, expansion, and churned revenue separately to give you an accurate picture.

Should one-time implementation fees be included in ARR?

No. ARR measures recurring revenue only. One-time fees—such as implementation, setup, training, or professional services—should always be excluded. Including them inflates your ARR and misrepresents the predictable portion of your revenue. Keep ARR clean by limiting it to revenue that repeats annually.

What is the difference between committed ARR and standard ARR?

Committed ARR (CARR) includes revenue from signed contracts that haven't started yet. Standard ARR only counts revenue from contracts that are currently active. CARR is useful for forecasting because it shows revenue that's locked in but not yet live. Most board reporting focuses on standard ARR, but both metrics have their place.

How do you calculate ARR for a multi-year contract?

Normalize the contract's recurring value to a single year by dividing the total recurring contract value by the number of years—so a $360,000 three-year subscription is $120,000 ARR. Exclude any one-time fees before you divide, since only the recurring portion belongs in ARR.

What is a good ARR growth rate?

It depends on your stage. Private B2B SaaS companies grew at a median of roughly 25% in 2024 according to SaaS Capital's 2025 benchmarks, with early-stage companies growing considerably faster and growth decelerating as ARR scales. Clean, contract-based ARR data is what makes a growth rate trustworthy enough to act on.