Between 2021 and 2024, 43% of SEC accounting fraud cases involved revenue recognition, according to the Anti-Fraud Collaboration's analysis. That number should concern every finance leader building on complex contract structures. For finance teams at B2B companies managing subscription, usage-based, or hybrid billing models, ASC 606 compliance demands more than understanding the rules — it requires operationalizing them across every contract, invoice, and revenue schedule. This guide breaks down the five-step revenue recognition framework and shows how modern finance teams can move from manual spreadsheet processes to automated, audit-ready workflows.

What is revenue recognition?

Revenue recognition is the accounting principle that determines when your company records revenue on its financial statements. It's not about when cash hits your bank account — it's about when you've actually earned that money by delivering what you promised to customers.

This distinction matters. When a customer pays upfront for an annual subscription, that cash isn't revenue yet. It sits on your balance sheet as deferred revenue — a liability representing the service you still owe. You only move that money to your income statement as you deliver the service over time.

For B2B companies with complex contracts, getting this right is the foundation of accurate financial reporting. And for modern finance teams managing subscription billing, usage-based pricing, or hybrid models, the complexity compounds quickly.

That's why modern Revenue Automation matters early — not just at audit time. Tabs sits downstream of CRM and CPQ to operationalize signed contracts. Rather than simply extracting contract data, Tabs uses AI-powered automation to understand the commercial intent of each agreement — classifying performance obligations, applying pricing logic, and generating billing and Revenue Recognition workflows that reflect what was actually sold.

What is ASC 606?

ASC 606 is the revenue recognition standard issued by the Financial Accounting Standards Board (FASB) that governs how companies report revenue from contracts with customers. It replaced a patchwork of industry-specific rules with a single, unified framework. The standard became effective for public entities for fiscal years beginning after December 15, 2017, with private companies required to adopt it one year later.

The standard applies to nearly every company that enters into contracts with customers. It aligns closely with International Financial Reporting Standards (IFRS) 15, making financial statements comparable across borders for global organizations.

Here's what makes ASC 606 different from earlier guidance:

- Principles over rules: Instead of rigid industry-specific requirements, ASC 606 uses a principles-based approach that requires judgment about when control transfers to the customer.

- Performance obligations: You must break contracts into distinct promises and recognize revenue as each promise is fulfilled — not when you send an invoice or receive payment.

- Variable consideration: Usage fees, discounts, and bonuses must be estimated and constrained to prevent revenue reversals.

For software-as-a-service (SaaS) and B2B companies, this creates real complexity. Deloitte's roadmap on ASC 606 notes that the impact on these entities may have been greater than on many other industry groups. A single contract might include software access, implementation services, and ongoing support — each requiring separate treatment under the standard.

Why does ASC 606 compliance matter?

Compliance builds the trust that enables growth — and the stakes go beyond avoiding penalties.

In fiscal year 2024, the SEC imposed $8.2 billion in financial remedies across enforcement actions — with revenue recognition errors among the most common triggers. These errors don't stay buried in footnotes. They surface during audits, delay fundraising, and destroy confidence.

According to PwC, revenue recognition is one of the accounting topics most scrutinized by investors and regulators. Inconsistent application creates material risk that can delay funding rounds, stall IPOs, or trigger costly restatements.

The consequences extend beyond finance:

- Board and investor confidence: Clean revenue recognition signals operational maturity. Messy books raise questions about what else might be wrong.

- Audit readiness: Auditors expect documented policies and consistent application across all contracts. Gaps mean findings.

- Comparability: Standardized reporting lets stakeholders compare your financials against peers without adjusting for accounting differences.

- Avoiding restatements: Revenue errors force costly corrections that erode trust and damage reputation.

For companies managing contracts with variable consideration, milestone payments, or usage-based components, manual processes create compliance risk that compounds as you scale. This is where Revenue Automation becomes essential — Tabs uses AI-powered automation to extract and classify contract terms and apply commercial context so Revenue Recognition follows the signed agreement.

ASC 606 revenue recognition in five steps

Every revenue transaction — regardless of industry or contract type — flows through the same five-step model. This framework forces you to deconstruct contracts into their economic components and recognize revenue only when the customer receives value.

TL;DR: Identify the contract, identify what you promised, determine the price, allocate that price across deliverables, and recognize revenue as you fulfill each promise.

Step 1: Identify the contract

A contract exists when there's an agreement that creates enforceable rights and obligations. Under ASC 606, this doesn't require a formal signed document — it can be written, oral, or implied by customary business practices.

But for revenue recognition purposes, the contract must meet specific criteria:

- Both parties have approved and committed to their obligations

- Each party's rights regarding goods or services are identifiable

- Payment terms are identifiable

- The contract has commercial substance

- Collection of consideration is probable

If these criteria aren't met, you can't recognize revenue — even if you've received cash. For example, if a customer's creditworthiness is doubtful at contract inception, you may need to defer recognition until payment is actually received.

Step 2: Identify performance obligations

Once you have a valid contract, you must identify the performance obligations within it. A performance obligation is a promise to transfer a distinct good or service to the customer.

This is often the most complex step for SaaS companies. KPMG's 2025 revenue handbook highlights how evolving business practices create new challenges when identifying performance obligations. Software contracts frequently bundle multiple items: the core platform with seat-based or enterprise licensing, premium features, training, and setup fees. You must determine which promises are distinct.

A promise is distinct if:

- The customer can benefit from the good or service on its own (or with readily available resources)

- The promise is separately identifiable from other promises in the contract

Common performance obligations in B2B contracts:

- Software subscription: The right to access the platform over the contract term

- Implementation services: Setup, configuration, or data migration

- Professional services: Training, consulting, or customization

- Support: Ongoing maintenance beyond standard bug fixes

If implementation is essential for the customer to use the software — meaning the software has no standalone value — those services aren't distinct. They'd be combined with the software into a single performance obligation.

Step 3: Determine the transaction price

The transaction price is the amount you expect to receive in exchange for transferring goods or services. For fixed-price contracts, this is straightforward. For contracts with variable components, it gets complicated.

Variable consideration includes usage-based fees, volume discounts, rebates, and performance bonuses. You must estimate these amounts using either the expected value method (probability-weighted average) or the most likely amount method.

Variable consideration may only be included to the extent that a significant revenue reversal is unlikely when the uncertainty resolves. This prevents companies from booking aggressive revenue estimates that later need to be reversed.

Other factors affecting transaction price:

- Significant financing component: If payment timing provides a financing benefit, adjust for the time value of money

- Non-cash consideration: Measure at fair value

For usage-based models, determining transaction price requires continuous re-estimation as actual usage data becomes available. This dynamic nature makes spreadsheets hard to maintain accurately at scale — especially when you need frequent re-estimation, audit trails, and controlled change management.

Step 4: Allocate the transaction price

When a contract contains multiple performance obligations, you must allocate the total transaction price to each based on relative standalone selling price (SSP). SSP is the price you'd charge if selling that item separately.

This prevents manipulation. Without allocation rules, companies could inflate prices on items delivered upfront while discounting items delivered over time — accelerating revenue recognition artificially.

Methods for estimating SSP when you don't have observable standalone sales:

| Method | When to use | How it works |

|---|---|---|

| Observable SSP | You sell the item separately | Use actual standalone selling price |

| Adjusted market assessment | Market data available | Estimate based on competitor pricing |

| Expected cost plus margin | Cost data is reliable | Add appropriate margin to costs |

| Residual approach | SSP is highly variable | Allocate the remaining price after allocating SSP to the other obligations |

Establishing SSP requires rigorous analysis of historical sales data. This allocation must be consistent and documented for auditors.

Step 5: Recognize revenue when obligations are satisfied

Revenue is recognized when you satisfy each performance obligation by transferring control to the customer. Control means the customer can direct the use of — and obtain the benefits from — the asset.

Recognition happens either at a point in time or over time. For most SaaS subscriptions, revenue is recognized over time because the customer consumes benefits continuously as you provide access.

You recognize over time if any of these criteria are met:

- The customer simultaneously receives and consumes benefits as you perform

- Your performance creates or enhances an asset the customer controls

- Your performance doesn't create an asset with alternative use, and you have an enforceable right to payment for work completed

Practical examples:

- SaaS subscription: Recognized ratably over the term (over time)

- Perpetual license: Recognized when delivered (point in time)

- Implementation: Depends on whether services are distinct — may be over time or bundled with subscription

Revenue Recognition software for ASC 606 compliance

Applying the five-step model manually becomes harder to control as contract volume grows — especially with amendments, variable consideration, and usage-based pricing. The result: slower closes, more tie-outs, and higher audit risk.

What to look for in ASC 606 software:

- Contract data extraction: Automatically capture key terms from signed contracts (for example, service periods, usage metrics, billing triggers, and renewal clauses) without manual re-keying

- Automated journal entries: Generate ASC 606-compliant entries based on contract and billing data

- Deferred revenue management: Track balances and schedules that update dynamically with amendments

- Audit trail: Complete traceability from contract to recognized revenue

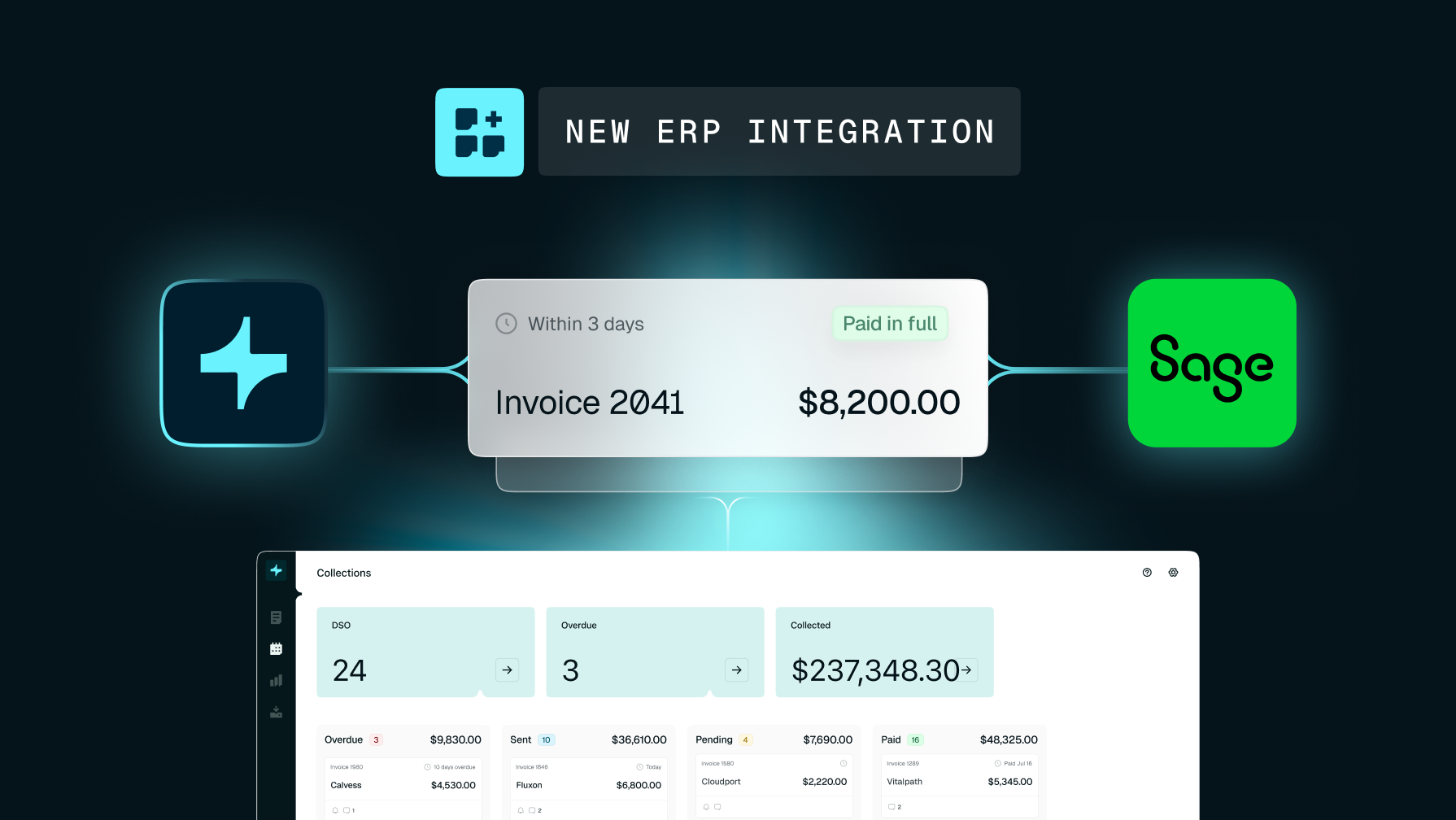

- ERP integration: Seamless sync with NetSuite, QuickBooks, or Sage Intacct

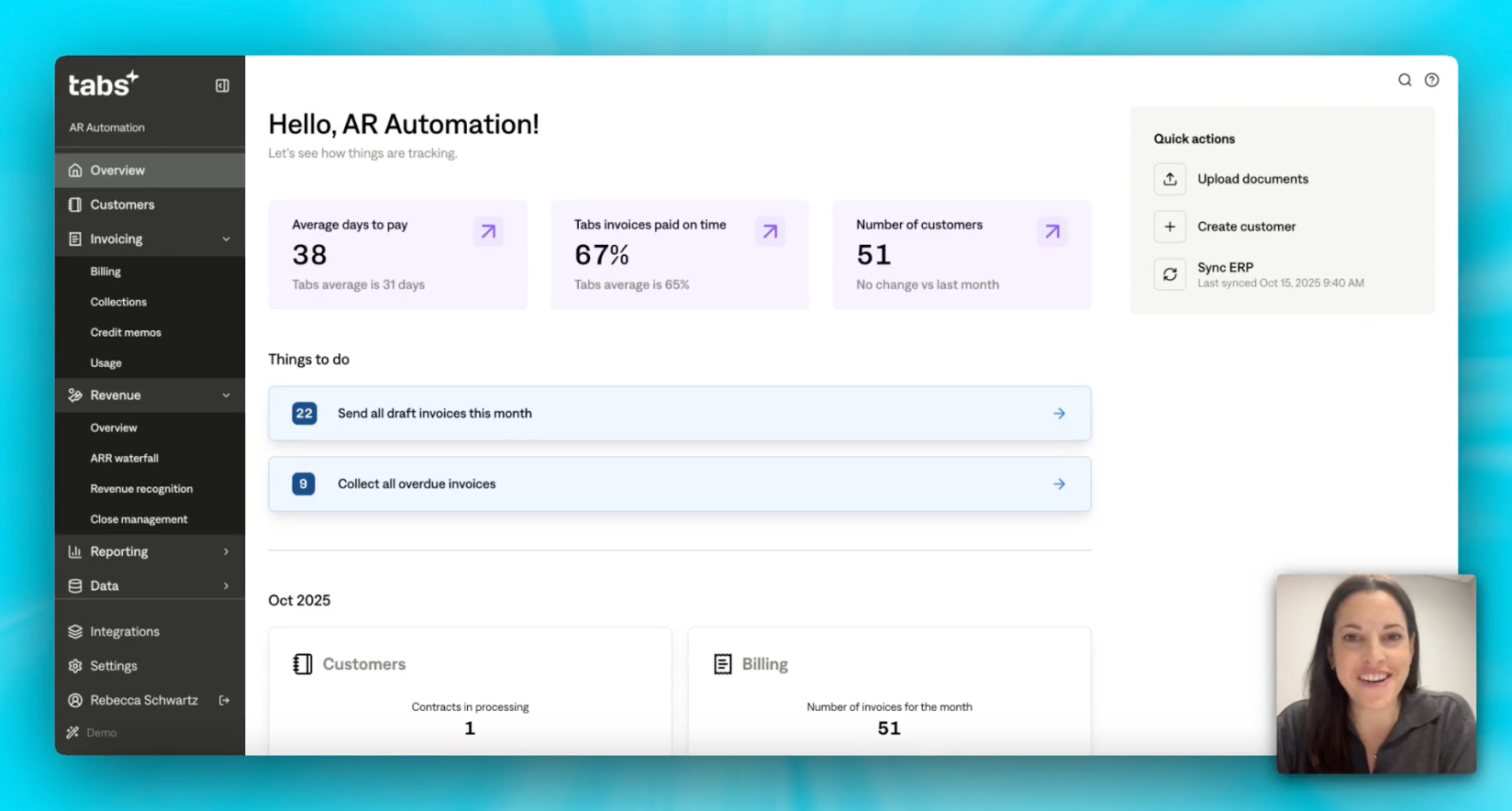

When manual processes break down at scale, automation should handle the full contract-to-cash workflow: extracting contract terms, classifying performance obligations, generating compliant revenue schedules, and syncing journal entries to your ERP — without requiring custom rules for each pricing model.

This is where Tabs differentiates. Tabs doesn't just extract contract data — it uses AI-powered automation to identify key terms (like pricing metrics, billing triggers, and service periods), classify the commercial structure, and translate that into accurate billing workflows and Revenue Recognition entries. Tabs operates as a system of intelligence for your contract-to-cash process, not just a system of record.

By unifying the Commercial Graph — the relationship between contracts, usage, and revenue — you eliminate the need to build complex spreadsheet models or reconcile across disconnected systems. Tabs connects contracts, billing events, and payment data to automate the entire process. You close faster with greater confidence.

Explore how Tabs can help you automate ASC 606 compliance and go live in

Frequently asked questions

What is ASC 606?

ASC 606 is the FASB revenue recognition standard that requires companies to recognize revenue using a five-step model based on when control of goods or services transfers to the customer.

What are the five steps of ASC 606?

The five steps are: identify the contract, identify performance obligations, determine the transaction price, allocate the transaction price, and recognize revenue when each obligation is satisfied.

When did ASC 606 go into effect?

ASC 606 became effective for public entities for fiscal years beginning after December 15, 2017, and for private companies for fiscal years beginning after December 15, 2018.

What is the difference between ASC 606 and ASC 605?

ASC 606 is a principles-based standard that replaced ASC 605's rules-based, industry-specific guidance with a single framework applicable across all industries.

How does ASC 606 apply to SaaS companies?

SaaS subscription revenue is typically recognized ratably over the contract term. Bundled contracts — such as those combining software access, implementation, and support — require separating each performance obligation and recognizing revenue independently. Learn more in our guide to SaaS revenue recognition software.

What is variable consideration under ASC 606?

Variable consideration includes amounts that depend on future events — such as usage fees, volume discounts, rebates, and performance bonuses — that must be estimated and constrained to prevent significant revenue reversals.