What is revenue recognition compliance?

Revenue recognition compliance is the process of recording revenue in your financial statements according to accounting standards like ASC 606 and IFRS 15. ASC 606 revenue recognition requires that you recognize revenue only when you've delivered value to a customer — not simply when cash hits your bank account or when you send an invoice.

The distinction matters. Cash-basis accounting records money when it arrives. Accrual-based accounting — what ASC 606 requires — records revenue when it's earned. For a SaaS company collecting $120,000 upfront for a one-year contract, compliance means recognizing $10,000 per month as you deliver the service — not $120,000 on day one.

For B2B finance teams managing complex contracts, compliance isn't just about following rules. It's about accurately reflecting your business reality. When your contracts include usage-based pricing, seat-based arrangements, bundled services, or milestone payments, simply booking invoice amounts as revenue leads to material misstatements. Modern revenue automation platforms like Tabs sit downstream of your CRM and configure, price, quote (CPQ) systems to operationalize signed contracts. Tabs uses trained models to classify clauses, normalize terms, and translate commercial context into accurate billing workflows and ASC 606-compliant revenue schedules — automatically and consistently.

ASC 606 and IFRS 15 revenue recognition standards

ASC 606 is the U.S. Generally Accepted Accounting Principles (U.S. GAAP) standard for revenue recognition, while International Financial Reporting Standards 15 (IFRS 15) is its international counterpart. Both standards converge on the same five-step model — before these standards, companies in different industries followed different rules, making financial comparisons difficult. Now, whether you're a software company in San Francisco or a manufacturing firm in Munich, you apply the same fundamental framework.

| Aspect | ASC 606 (U.S. GAAP) | IFRS 15 (International) |

|---|---|---|

| Applies to | Public and private U.S. entities | Entities reporting under IFRS |

| Core model | Five-step framework | Five-step framework (identical) |

| Disclosure requirements | Extensive quantitative and qualitative | Similar, with presentation variations |

| License guidance | Detailed implementation rules | More principles-based |

While the core principles align, implementation details differ. ASC 606 provides more prescriptive guidance for software licenses and intellectual property. IFRS 15 relies more heavily on judgment. For B2B companies with hybrid pricing models, both standards demand rigorous documentation of how you identify performance obligations and allocate transaction prices.

Why revenue recognition compliance matters for finance leaders

Compliance isn't a checkbox exercise — PwC's accounting change survey found 71% of public companies reported contract reviews somewhat or very difficult. It directly impacts your audit outcomes, investor confidence, and operational efficiency.

Misstatements create real consequences. Recognize revenue too early, and you inflate current performance while borrowing from future periods. Recognize it too late, and you understate growth. Either direction erodes trust with the people who matter — board members, investors, and lenders who rely on accurate financials to make decisions.

The operational burden compounds the problem. Finance teams stuck in manual compliance processes spend days reconciling spreadsheets instead of analyzing strategic initiatives. Every hour spent re-keying contract terms or chasing down billing discrepancies is an hour not spent on forward-looking work.

- Audit findings: Errors trigger increased scrutiny, qualified opinions, or forced restatements

- Investor trust: Inconsistent reporting undermines confidence in your financial data

- Operational drag: Manual rework consumes bandwidth that should go toward strategy

- Forecasting errors: Revenue timing mismatches distort pipeline visibility and cash flow projections

Who must comply and when revenue recognition rules apply

ASC 606 applies to any entity entering contracts to transfer goods or services to customers. Public companies, private companies, nonprofits — if you generate revenue from customer contracts, you must comply.

For public companies, ASC 606 took effect for fiscal years beginning after December 15, 2017. Private companies and nonprofits followed one year later, with an effective date of December 15, 2018.

But not every business transaction qualifies as a contract under the standard. To fall within scope, an agreement must meet five specific criteria. If it doesn't, you cannot recognize revenue — even if you've already received payment.

- Approval and commitment: All parties have approved the contract and committed to their obligations

- Identification of rights: You can identify each party's rights regarding goods or services

- Clear payment terms: The contract specifies payment terms

- Commercial substance: The contract changes the risk, timing, or amount of your future cash flows

- Probable collection: You expect to collect the consideration you're entitled to

This often trips up early-stage companies. Collecting a non-refundable deposit doesn't mean you can recognize revenue. Without a formal contract meeting all five criteria, that cash sits on your balance sheet as a liability until you've established enforceable rights.

The five-step model for ASC 606 revenue recognition

The five-step model is the operational core of ASC 606. It guides you from contract signature to revenue recognition, forcing you to break complex agreements into their component parts.

1. Identify the contract

First, confirm a valid agreement exists by verifying the five criteria above. In B2B environments, this gets complicated. Master service agreements with multiple order forms, amendments, and side letters must be evaluated together if they were negotiated with a single commercial objective.

Why it matters: Treating related agreements as separate contracts when they should be combined — or vice versa — changes how you allocate and recognize revenue.

2. Identify performance obligations

A performance obligation is a promise to transfer a distinct good or service. You must assess whether bundled items — software, training, maintenance — are distinct from each other. If a customer can benefit from an item on its own, and it's separately identifiable from other promises, it's a separate performance obligation.

Why it matters: Missing a distinct obligation means you'll recognize revenue on the wrong schedule.

3. Determine the transaction price

The transaction price is the consideration you expect to receive. For fixed-price contracts, this is straightforward. For modern B2B models with usage-based components, volume discounts, or performance bonuses, you must estimate variable consideration and update those estimates each reporting period.

Why it matters: Underestimating variable consideration understates revenue; overestimating creates reversal risk.

4. Allocate the transaction price

Once you have the total price and list of obligations, allocate the price to each obligation based on its standalone selling price (SSP). If you sell a $100,000 subscription that includes $20,000 of free implementation, you can't recognize $100,000 for the software alone. You must allocate proportionally.

Why it matters: Incorrect allocation shifts revenue between periods and performance obligations.

5. Recognize revenue

You recognize revenue as you satisfy each performance obligation by transferring control to the customer. For SaaS subscriptions, control transfers over time — recognize ratably. For perpetual licenses or hardware, control may transfer at a point in time — recognize immediately.

Why it matters: This final step determines when revenue hits your income statement.

How contract modifications affect revenue recognition

B2B contracts rarely stay static. Customers upgrade seats mid-term, add new product lines, renegotiate pricing, or extend agreements — and each change can alter how you recognize revenue under ASC 606. A contract modification is any change to the scope, price, or both that all parties have approved.

ASC 606 prescribes three distinct treatments depending on the nature of the change. First, if the modification adds distinct goods or services at their standalone selling price, you treat it as a separate contract — the original agreement's accounting stays untouched. Second, if the remaining goods or services are distinct from what you've already delivered but not priced at SSP, you account for it as a termination of the old contract and creation of a new one, reallocating the combined remaining consideration. Third, if the remaining goods or services are not distinct from what was already transferred, you apply a cumulative catch-up adjustment — recalculating revenue from inception and booking the difference in the current period.

This is where complexity compounds for B2B companies. Multi-year agreements with quarterly amendment cycles, usage-tier adjustments, and mid-term scope changes can trigger dozens of modification assessments per contract. Each one requires you to evaluate distinctness, recalculate allocation, and update variable consideration estimates. Without systematic tracking, modifications become a leading source of misstatements and audit findings.

Common revenue recognition scenarios in B2B contracts

The five-step model sounds clean in theory. In practice, B2B contracts rarely fit neatly into a single category.

- Subscription contracts: You recognize subscription revenue ratably over the term — for example, you recognize a 12-month subscription evenly across the service period, regardless of when cash arrives.

- Usage-based pricing: You recognize revenue as consumption occurs. This requires accurate metering and real-time accrual processes.

- Hybrid models: Fixed subscription fees recognized ratably; variable usage fees recognized as incurred. Separating these components requires sophisticated allocation logic.

- Bundled services: Implementation services may combine with software into a single obligation (if highly customized) or separate into distinct obligations (if standard).

- Milestone payments: You recognize milestone-based revenue only when you achieve the milestone and the customer accepts the deliverable.

Each scenario demands different treatment. And when your contracts blend multiple models — a subscription with usage overages and implementation services — the complexity multiplies.

Implementation roadmap for revenue recognition compliance

Why it matters: ASC 606 compliance is an ongoing operational requirement, not a one-time project. A structured five-phase approach prevents gaps that surface during audits.

Achieving compliance isn't a one-time project — Deloitte notes ASC 606 requires greater judgment than legacy guidance, resulting in higher ongoing costs. It's an ongoing operational requirement that demands a structured approach.

- Phase 1 — Assessment: Inventory existing contracts. Identify standard terms and non-standard clauses that pose compliance risks — usage tiers, volume discounts, termination-for-convenience provisions, and automatic renewal language. Document current policies, map them against ASC 606 requirements, and identify gaps that need resolution before you can design new policies.

- Phase 2 — Policy design: Establish clear accounting policies for standalone selling prices, variable consideration estimates, and contract modifications. Define your SSP estimation methods — adjusted market assessment, expected cost plus margin, or residual approach — and document the rationale for each. Build consistent documentation templates so policy decisions are auditable from day one.

- Phase 3 — System readiness: Evaluate whether your current tools can capture the data ASC 606 demands: contract start and end dates, performance obligation details, usage data feeds, variable consideration inputs, and modification history. Manual data entry introduces high error risk. Map every required data field to a system source, and flag any gaps that require new integrations or process changes before go-live.

- Phase 4 — Controls and testing: Implement internal controls around the key judgment areas: SSP calculations, transaction price allocation accuracy, and timing of performance obligation satisfaction. Run parallel calculations comparing automated results against your prior approach. Test edge cases — mid-term upgrades, early terminations, and usage-based true-ups — to validate that your system handles them correctly.

- Phase 5 — Auditor coordination: Involve external auditors early. Share technical accounting memos, policy documents, and system documentation before the audit begins — not during it. Early alignment on your methodology for SSP estimation, variable consideration constraints, and modification treatment reduces the risk of surprises during fieldwork and keeps your close timeline on track.

How Tabs automates revenue recognition compliance

Why it matters: As contract volume grows and pricing models evolve, manual compliance processes break down. Tabs automates the full cycle — from contract ingestion to audit-ready journal entries.

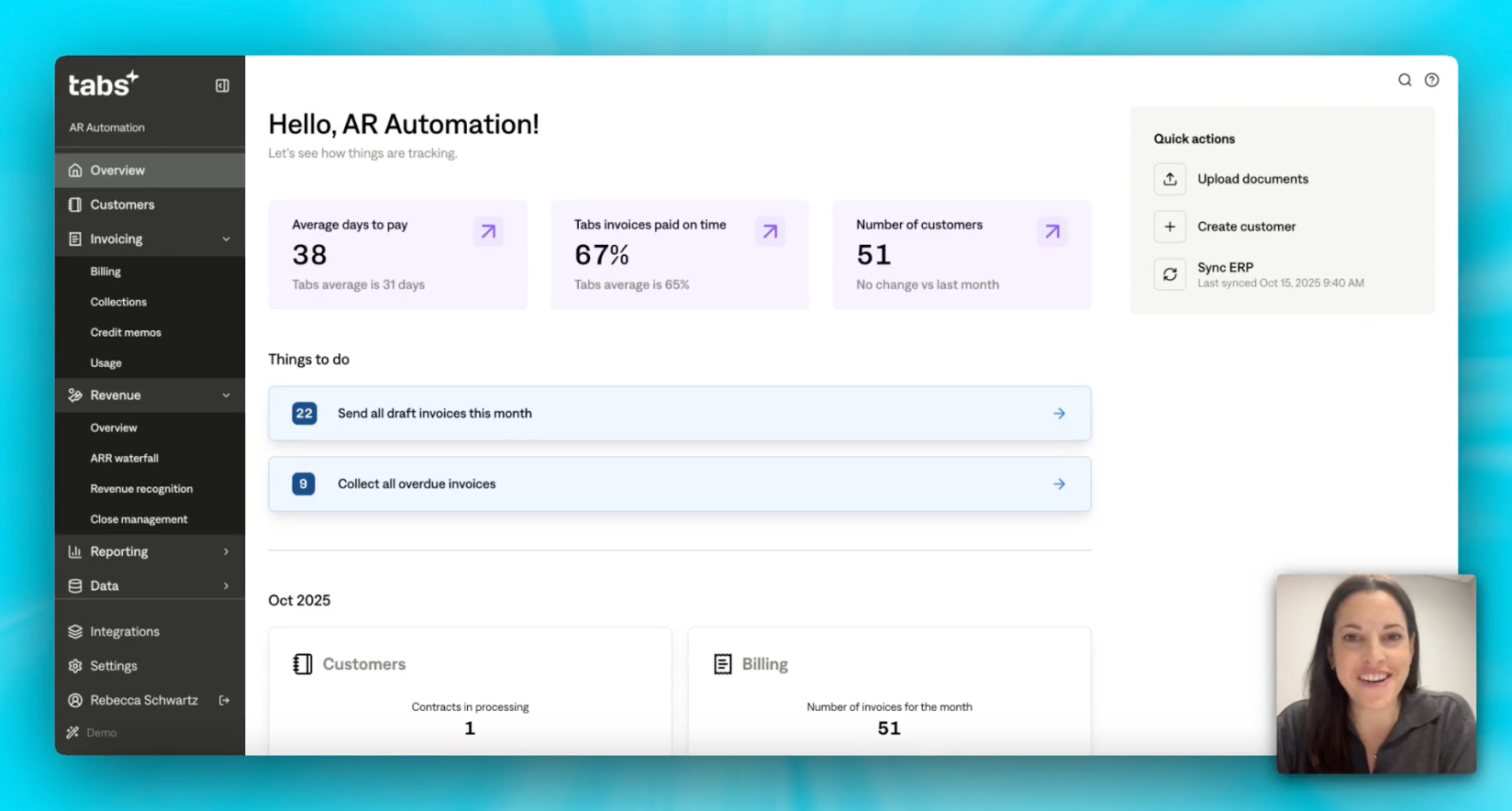

Manual compliance can work for small companies with simple contracts. But as transaction volume grows and pricing models evolve, manual processes struggle to keep pace — Statsig, for example, eliminated aged receivables entirely and scaled to 3x invoice volume without adding headcount after moving to automated revenue operations. Modern revenue recognition software can close this gap. Tabs serves as an AI-powered revenue automation platform that transforms compliance from a manual burden into an automated, audit-ready process.

Unlike generic tools that only extract text, Tabs uses trained models to identify key clauses and structured terms, then maps them to the operational outcomes finance cares about — billing schedules, contract changes, and ASC 606 Revenue Recognition treatment. It doesn't just capture what a contract says — it extracts and classifies the terms, maps them to billing workflows and ASC 606-compliant revenue schedules, and flags non-standard clauses for review when they can change accounting conclusions.

AI contract ingestion and structured terms

Tabs automatically extracts billing terms and pricing structures from executed agreements — PDFs, Word documents, and attached order forms captured via email — and structures the inputs you use to identify performance obligations under your ASC 606 policies. Tabs uses trained models to classify terms and route them appropriately — for example, it tags "net 30" as a collections and cash-timing input (not a revenue-timing driver) and flags clauses like "cancel for convenience" because they can affect enforceable rights, contract term, and the Revenue Recognition analysis under ASC 606.

Why it matters: Eliminates manual contract review and ensures non-standard terms don't slip through the cracks.

Automated invoicing and hybrid billing

Once contract data is structured, Tabs generates invoices automatically. Tabs supports subscriptions, usage-based pricing, and hybrid arrangements without manual intervention or custom scripts.

- Subscription billing: Recurring invoices generated based on contract-specific start and end dates

- Usage-based billing: Consumption data ingested and billed according to contracted rates and tiers

- Hybrid models: Fixed and variable components handled on a single invoice

Why it matters: Accurate billing data flows directly into revenue recognition without re-keying.

ASC 606 rules engine and variable consideration

Tabs includes a purpose-built rules engine that applies ASC 606 logic automatically. It allocates transaction prices across performance obligations based on standalone selling prices, handles variable consideration dynamically, and processes contract modifications correctly.

Why it matters: Tabs recognizes revenue in the right period without manual calculations or spreadsheet risk.

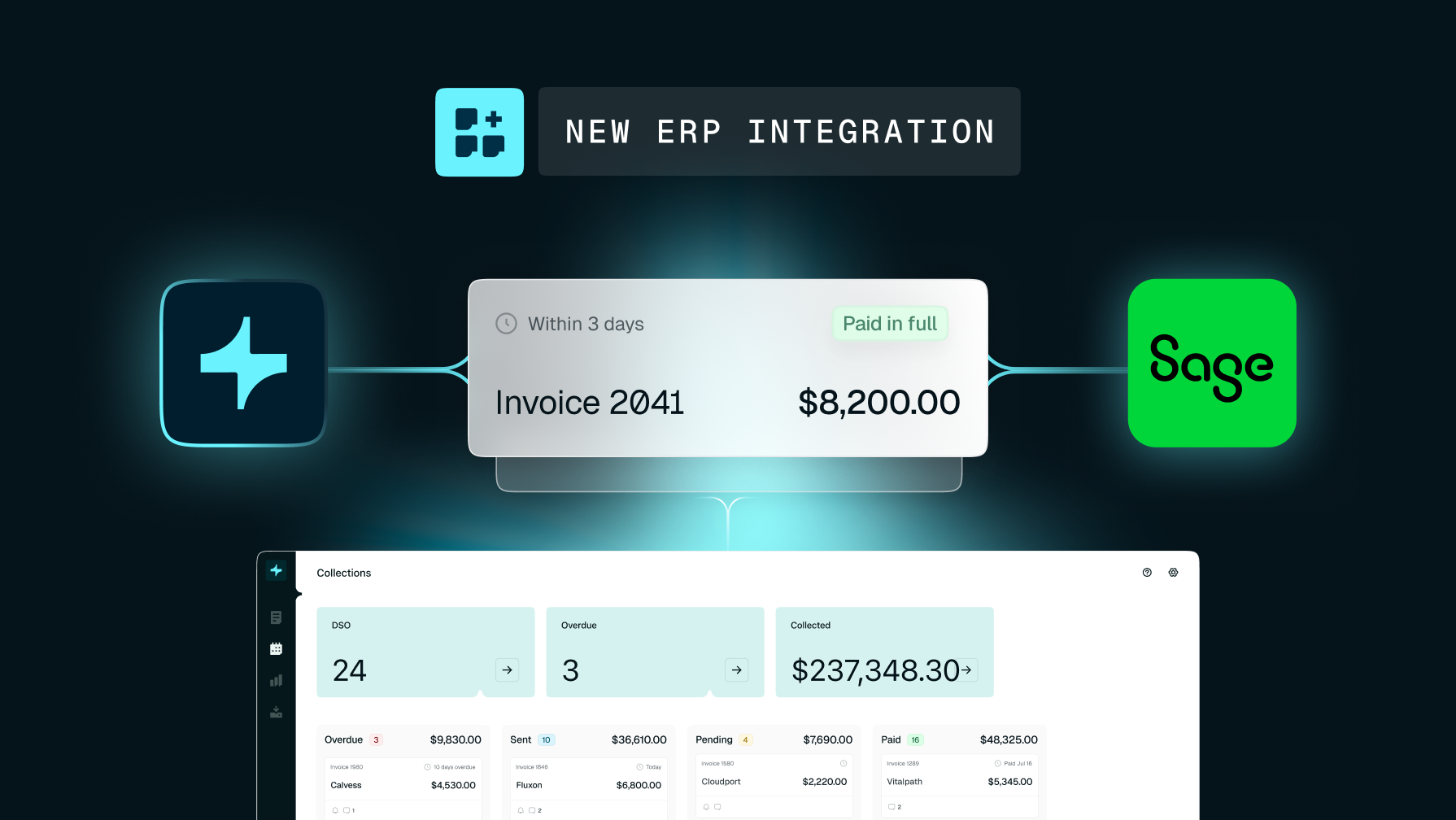

Audit-ready reporting and enterprise resource planning (ERP) integration

Tabs maintains a complete, time-stamped, tamper-evident audit trail. Every contract ingestion, invoice, and revenue entry is logged with timestamps. Integrations with NetSuite, QuickBooks, and Sage Intacct can push journal entries directly into your general ledger.

Why it matters: Auditors get the documentation they need without weeks of manual preparation.

Frequently asked questions

How does ASC 606 handle usage-based billing with variable monthly consumption?

Automated systems ingest consumption data on a defined cadence (for example, daily or near real time), apply contracted rates, and accrue revenue as usage occurs rather than waiting for invoice dates. That helps you recognize revenue in the appropriate period based on your metering data and close timeline.

What documentation do auditors require from an automated revenue recognition system?

Auditors expect a complete audit trail linking revenue entries back to original contracts and billing events, plus system configuration logs, user access controls, and change history verifying that rules were applied consistently.

What are the five steps of revenue recognition under ASC 606?

The five steps are: (1) identify the contract, (2) identify performance obligations, (3) determine the transaction price, (4) allocate the transaction price to each performance obligation, and (5) recognize revenue as each obligation is satisfied. For a detailed breakdown with B2B-specific examples, see the five-step model section above.

When did ASC 606 go into effect?

ASC 606 took effect for public companies in fiscal years beginning after December 15, 2017, and for private companies and nonprofits in fiscal years beginning after December 15, 2018.

How does ASC 606 differ from IFRS 15?

Both standards share the same five-step revenue recognition framework, but they diverge on implementation details — ASC 606 provides more prescriptive guidance on software licenses and collectibility thresholds, while IFRS 15 takes a more principles-based approach and differs in its treatment of contract costs. See the ASC 606 and IFRS 15 comparison section above for a detailed breakdown.