Cash flow reporting: A complete guide for finance teams

For finance teams managing complex B2B revenue workflows, cash flow reporting is the clearest measure of whether your business model actually works. This guide breaks down the components, methods, and step-by-step process for building accurate cash flow reports, and shows how modern revenue automation transforms reporting from a monthly scramble into real-time visibility.

What is cash flow reporting?

Cash flow reporting is the process of tracking all cash moving into and out of your business over a specific period. It shows you the difference between what your income statement says you earned and what actually landed in your bank account.

This distinction matters more than most finance leaders realize. A company can show strong profits on paper while running dangerously low on cash—especially in B2B environments where payment terms stretch 30, 60, or even 90 days. PwC's Working Capital Study found DSO has risen 5.7% over the past decade, exacerbating this timing gap.

Cash flow reporting strips away the accounting abstractions and answers a simple question: do we have the money to operate?

For B2B finance teams managing complex billing models—subscription revenue, usage-based pricing, milestone payments—this visibility becomes critical. Revenue recognition timing often diverges significantly from when cash actually arrives. Your income statement might show $500,000 in recognized revenue this quarter, but if half of that sits in accounts receivable (AR), your cash position tells a very different story.

Modern revenue automation platforms like Tabs address this gap by operationalizing signed contracts downstream of your CRM and CPQ—turning contract terms into billing, collections, and cash forecasting that reflects how customers actually pay. Rather than waiting until month-end to discover cash flow surprises, you get real-time visibility into what's been invoiced, what's been collected, and what's still outstanding.

Cash flow reporting components

Every cash flow report divides into three sections: operating activities, investing activities, and financing activities. Each section isolates a different type of cash movement, giving you granular insight into where money comes from and where it goes.

Operating activities

Operating activities capture cash generated from your core business. This includes cash received from customers, cash paid to suppliers and employees, and payments for interest and taxes.

For B2B companies with recurring revenue, this section reveals how effectively you convert invoices into collected cash. Positive operating cash flow means your day-to-day business sustains itself. Negative operating cash flow—even with strong revenue—often signals collection problems or pricing issues rather than weak sales.

- Cash received from customers: Actual inflows from sales, distinct from recognized revenue

- Cash paid to suppliers and employees: Outflows for payroll, software, inventory, and vendor payments

- Interest and taxes paid: Mandatory outflows for debt service and government obligations

Why it matters: Operating cash flow is the truest measure of whether your business model actually works.

Investing activities

Investing activities track cash used for or generated from long-term assets. This includes purchasing equipment, acquiring other businesses, or selling assets you no longer need.

Negative cash flow here isn't necessarily bad. It often indicates you're reinvesting in growth—buying equipment, capitalizing eligible internal-use software, or acquiring long-lived assets to expand infrastructure. The key is ensuring these investments generate adequate returns over time.

Why it matters: This section shows whether you're building for the future or liquidating to survive.

Financing activities

Financing activities cover cash movements related to debt, equity, and dividends. This includes raising capital through loans or stock issuance, repaying debt, or distributing profits to shareholders.

A company showing positive cash flow primarily from financing activities—like a fresh venture round—is in a fundamentally different position than one generating cash from operations. This section reveals your reliance on external capital versus organic growth.

Why it matters: Financing activities show how you fund the business and return value to stakeholders.

Cash flow reporting methods

Two approaches exist for preparing the operating activities section: the direct method and the indirect method. Both yield the same total, but they arrive there differently.

The indirect method starts with net income and adjusts for non-cash items and working capital changes. This is the industry standard because it uses data already in your general ledger. You add back depreciation, subtract increases in accounts receivable, and add increases in accounts payable to reconcile net income to actual cash flow.

The direct method lists actual gross cash receipts and payments—"cash received from customers" and "cash paid to suppliers." While accounting standards often recommend this approach for its clarity, few companies use it. Tracking every individual cash transaction requires detailed systems that most finance teams lack.

| Aspect | Direct method | Indirect method |

|---|---|---|

| Starting point | Gross cash receipts and payments | Net income |

| Complexity | Higher—requires detailed cash tracking | Lower—uses existing accrual data |

| Adoption | Less common | Industry standard |

| Insight | Shows actual cash sources | Shows reconciliation adjustments |

Automate cash flow reporting with Tabs

How to create a cash flow report step-by-step

Building a cash flow report manually requires pulling data from your balance sheet and income statement, then reconciling the differences. Most teams use the indirect method. Here's how it works.

Step 1: Determine the starting balance

Begin with your cash and cash equivalents balance at the start of the reporting period. This figure must match the ending balance from your previous period's balance sheet exactly.

If these numbers don't align, you have a reconciliation error upstream. According to Deloitte, cash flow statement errors continue to cause restatements and SEC scrutiny, making clean starting data non-negotiable.

Why it matters: Every subsequent calculation builds on this foundation—errors here cascade through the entire report.

Step 2: Calculate cash flow from operating activities

Start with net income from your income statement. Then adjust to convert from accrual basis to cash basis.

First, add back non-cash expenses that reduced net income but didn't touch cash: depreciation, amortization, stock-based compensation. These are accounting entries, not actual outflows.

Next, adjust for working capital changes:

- Accounts receivable increase: Subtract from net income (you recognized revenue but haven't collected it)

- Accounts payable increase: Add to net income (you incurred expenses but haven't paid them)

- Inventory changes: Adjust based on whether you're building or depleting stock

For B2B companies, the AR adjustment often reveals the biggest driver of cash variance—how quickly customers actually pay relative to what you recognized. If your AR balance grew by $100,000 this month, you subtract that amount—reflecting that while you booked the revenue, the cash hasn't arrived.

Why it matters: This step exposes the gap between paper profits and actual liquidity.

Step 3: Calculate cash flow from investing and financing activities

For investing activities, subtract cash spent on asset purchases and add cash received from asset sales. For financing activities, add cash from loans or equity raises and subtract cash used for debt repayment or dividends.

Sum all three sections to determine your net change in cash. Add this to your beginning balance to arrive at your ending cash position. This final number must match your balance sheet. If it doesn't, investigate immediately.

Why it matters: The ending balance is your proof of accuracy—it either reconciles or it doesn't.

Why cash flow reporting matters for finance teams

Cash flow reporting moves beyond compliance into strategic territory. While your income statement tracks performance, your cash flow report tracks survival.

- Forecasting accuracy: According to EY, companies are three times as likely to miss cash flow forecasts than revenue targets—making accurate cash flow data essential for grounding projections in reality

- Covenant compliance: Lenders often require specific cash flow metrics—accurate reporting prevents technical defaults

- Capital allocation: Knowing your actual cash position enables confident investment decisions

- Board and investor confidence: Clean cash flow reporting signals operational maturity

The bottom line: Profitability doesn't pay bills—cash does. A company can show strong revenue growth while struggling to make payroll if collections lag behind invoicing.

Cash flow analysis indicators and red flags

Reading a cash flow report requires looking beyond raw numbers to understand the story they tell.

Healthy indicators:

- Operating cash flow consistently positive

- Operating cash flow (OCF) growing in line with or faster than net income

- Cash conversion cycle stable or improving

Red flags:

- Net income positive but operating cash flow negative

- AR growing faster than revenue (collection issues)

- Increasing reliance on financing activities to fund operations

When a company consistently reports profits but negative operating cash flow, those profits are "low quality"—tied up in uncollected receivables or unsellable inventory. This pattern often precedes liquidity crises.

Cash flow reporting vs other financial statements

The cash flow report works alongside your income statement and balance sheet, but each serves a different purpose.

Your income statement shows profitability on an accrual basis—revenue when earned, expenses when incurred. Your balance sheet shows financial position at a single point in time. Your cash flow report bridges the gap by showing actual cash movement over the period.

| Statement | What it shows | Key question answered |

|---|---|---|

| Income statement | Profitability | Are we profitable? |

| Balance sheet | Financial position | What do we own and owe? |

| Cash flow report | Cash movement | Do we have cash to operate? |

All three are necessary for a complete picture. The cash flow report often reveals truths that accrual accounting obscures.

Automation for cash flow reporting with AI

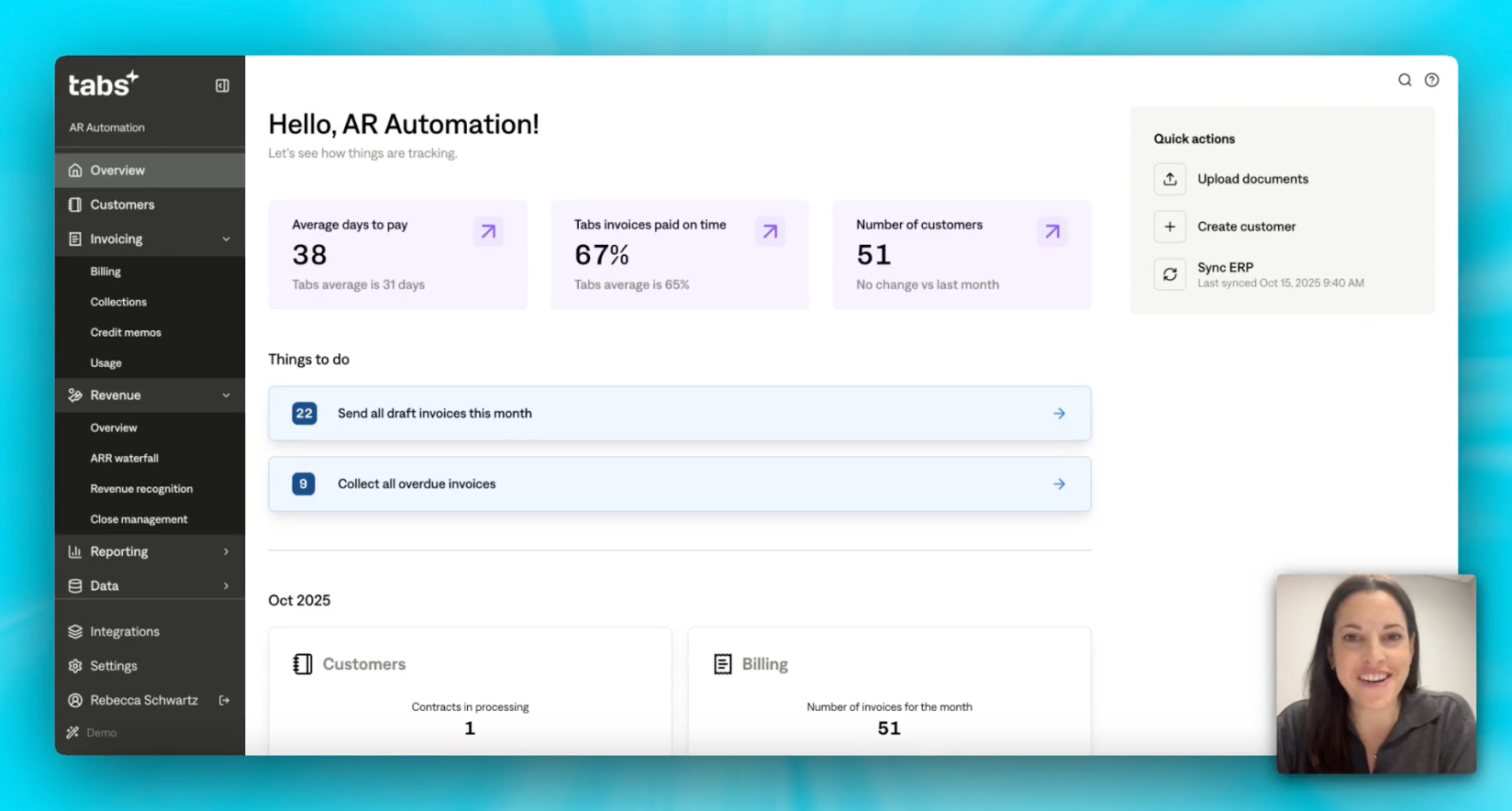

Traditional cash flow reporting is manual and reactive. Finance teams spend days each month exporting data from CRM, billing tools, and bank portals, then stitching it together in spreadsheets. By the time the report is finished, the data is already stale.

Tabs transforms this process by automating the contract-to-cash lifecycle. Instead of manually re-keying deal terms and reconciling after the fact, Tabs uses AI to extract and interpret signed contract terms, generate invoices aligned to those terms, and track collections in real time.

The difference isn't just speed—it's commercial context. Tabs doesn't merely move data from point A to point B. Using trained models, Tabs interprets contract terms (pricing, credits, renewals, and billing triggers) and operationalizes them into billing workflows and revenue recognition-ready outputs. This means the "cash received" portion of your operating activities reflects what's been invoiced and collected to date—grounded in transaction data rather than spreadsheet assumptions.

- Eliminate manual data entry: Invoices generate directly from signed contracts

- Real-time AR visibility: Track what's invoiced, collected, and outstanding without waiting for month-end

- Faster reconciliation: Payment data matches automatically to invoices

- Accurate forecasting: Predict when cash will actually land based on historical payment behavior and contract terms

When your billing and collections data is clean at the source, cash flow reporting becomes a byproduct of good operations rather than a monthly scramble.